CBAM Regulation adopted

Written By

Following a turbulent legislative process, Regulation (EU) 2023/956 of the European Parliament and of the Council of 10 May 2023 establishing a carbon border adjustment mechanism (or the CBAM) was published in the Official Journal of the European Union on 16 May 2023. Below we explain how the system around the CBAM is expected to work, and how to prepare for the new obligations it brings.

Coverage

The CBAM will cover imports of selected goods, identified using CN codes, from those sectors deemed to pose the highest risk of carbon leakage: cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. It will mainly apply to the basic materials produced in those sectors, with the exception of the steel sector, where it will also cover more refined materials produced further down value chains (such as screws and bolts).

The CBAM will cover both direct and indirect emissions embedded in imported goods, apart from goods that are covered by the indirect cost compensation schemes under the EU ETS – in such cases, only direct emissions will be accounted for.

| Sector | Greenhouse gas |

| Iron and steel | Carbon dioxide |

| Aluminium | Carbon dioxide and perfluorocarbons |

| Hydrogen | Carbon dioxide |

| Fertilisers | Carbon dioxide and nitrous oxide |

| Electricity |

Carbon dioxide |

| Cement |

Carbon dioxide |

Transitional phase

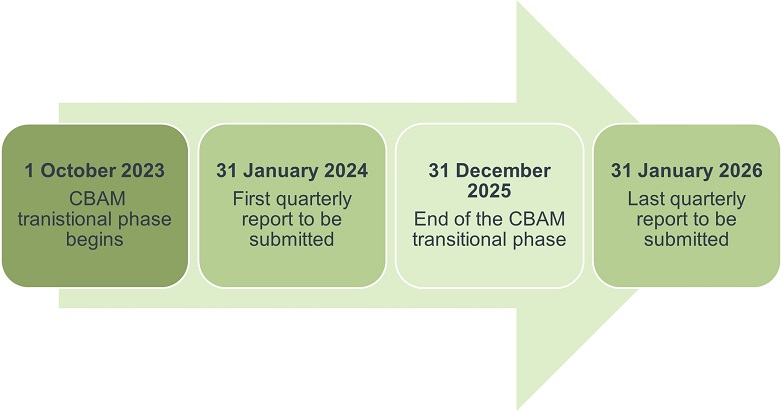

Before the CBAM becomes fully operational, there will be a transitional period. Most notably, during this period there will be no obligation to purchase CBAM certificates – i.e., initially, financial adjustments will not be enforced. This period will run from 1 October 2023 to 31 December 2025. Its aim is to provide an opportunity to fine-tune the whole system around the CBAM, test and develop methodologies, and gather and analyse relevant data. Also, the transitional period will help create awareness among customs declarants concerning the new obligations, and will give them time to prepare before the “definite” phase of the CBAM kicks in.

The key obligation during the transitional period is quarterly reports, which will only need to include the emissions embedded in goods imported in the preceding quarter of the year and the carbon price effectively paid in the country of origin. While there will be no financial adjustments at this stage, these reporting obligations should not be neglected. Any inconsistencies between data reported during the transitional period and later, once the CBAM becomes fully effective, are very likely to draw the authorities’ attention and cause them to investigate further. That is why it is crucial to take a consistent strategic approach from the very beginning.

Quarterly reports during the transitional phase must be submitted by no later than one month after the end of each quarter, i.e. the first report should be submitted by 31 January 2024 and the last by 31 January 2026.

CBAM certificates

Once the transitional phase is over, the CBAM will involve not just reporting obligations, but financial ones as well. For this purpose, a system of CBAM certificates will be set up.

In some ways, these certificates will resemble the allowances used under the EU ETS – each of them will represent one metric tonne of emissions embedded in goods, and their prices will be strictly correlated. The price of CBAM certificates will be defined as the average of the closing prices of the EU ETS allowances on the auction platform for each calendar week. Yet there are some notable differences - while the EU ETS sets a limit on the total number of allowances issued (a cap), the CBAM has no predetermined number of certificates to sell, since such a limit would effectively constitute a limit on imports. There is also no secondary market for certificates, as this could lead to a situation where their prices no longer reflect the prices of EU ETS allowances.

Authorisation procedures

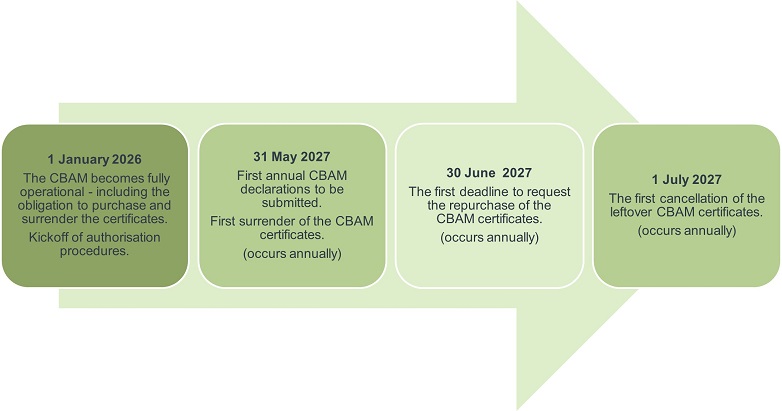

In general, once the CBAM becomes fully applicable on 1 January 2026, goods listed in Annex I to the CBAM Regulation can only be imported into the customs territory of the EU by Authorised Declarants. To be granted this status, importers will have to submit a relevant application. Importers established outside the EU cannot submit such a declaration and need to act through an indirect customs representative. For EU-based businesses, using such representative is possible, but not mandatory.

Authorisation is conditional upon meeting specific conditions. Most notably:

- the applicant must not have committed a serious or repeated infringement of customs, tax or market abuse regulations during the five years preceding the application;

- the applicant should demonstrate it has the financial and operational capacity to fulfil its obligations under the CBAM – in cases where the applicant was not established throughout the two financial years preceding the year of applying for authorisation, it must provide a guarantee.

Declarations and cancellation of certificates

Once the CBAM becomes fully operational, quarterly reports submitted during the transitional phase will be replaced by annual CBAM Declarations. These declarations should be submitted by 31 May each year to cover the previous year, meaning that the first CBAM declaration, in respect of the calendar year 2026, should be submitted by 31 May 2027. A CBAM Declaration should include information on the total amount of imported goods, their embedded emissions, verification reports, and information on any applicable adjustments.

CBAM certificates must also be surrendered by 31 May each year. The number of certificates surrendered should correspond to the data disclosed in the CBAM Declaration.

In this context, it is important to consistently track the total number of emissions embedded in imported goods throughout the year since:

- only one third of the total number of CBAM certificates purchased by the Authorised CBAM Declarant during the previous calendar year can be repurchased by the authorities – and any certificates left after the repurchase will be cancelled and cannot be used in the following year; and

- there is an obligation to keep a sufficient number of certificates each quarter (corresponding to at least 80% of the embedded emissions in imported goods).

International response

Ever since plans to introduce this mechanism emerged, opponents have argued that it is incompatible with World Trade Organization (WTO) rules as it constitutes a barrier to trade – some have called it a form of disguised “green protectionism”. This issue has been the subject of much heated debate. The CBAM’s proponents argue that it is non-discriminatory (since the financial and administrative burdens imposed on imports apply equally to domestic producers) and fully compliant with WTO rules.

The countries expected to be the most affected by the CBAM include China, the United Kingdom, Turkey, India, and the United States. It had also been anticipated that Russia and Ukraine would be among those most affected, but due to the destruction of Ukrainian industry and the sanctions on Russia since the war in Ukraine broke out, this is no longer the case.

The CBAM could be contested under the WTO framework for being non-compliant with the rules on the freedom of international trade. There have been reports that both China and India are considering such a move.

Therefore, some changes to the CBAM might be needed to ensure WTO compatibility, should challenges by those third countries prove successful.

Further action

While the recently published CBAM provides a framework for how the CBAM system is to function, many elements, usually more technical ones, will be regulated by delegated and implementing acts, which need to be developed by the European Commission in a timely manner.

The first implementing regulation to be adopted concerns reporting obligations during the transitional period. The Commission launched a consultation on the draft act on 13 June 2023.

The draft provides:

- a description of the reporting obligations – which include types and quantity of goods, their country of origin, the installation where they were produced, and the production routes used;

- flexible calculation methods, allowing for methods such as continuous measurement systems, calculations based on source streams or, by a way of a derogation until the end of 2024, any other method used under the applicable domestic MRV systems;

- rules on reporting the carbon price paid in the country of origin;

- setting up an electronic database for collecting reported information - the CBAM Transitional Registry together - with detailed rules for its functioning, including interoperability with existing customs systems.

Consultations on the draft are expected to last until 11 July 2023. As mentioned above, this is the first in a series of consultations on the implementing and delegated regulations, so it is important to keep a close eye on any developments not to miss a chance to provide feedback.

How to prepare

- Agree on a strategic approach towards the CBAM from the very beginning of the transitional phase. Analyse carbon footprints across value chains. Consider reviewing investment strategies.

- Draft the relevant documentation (such as a motion for authorisation) in advance.

- Get in touch with operators of installations in third countries – address the issue of data collection and verification, including associated costs. Analyse and negotiate contracts with suppliers.

- Engage in the public consultations concerning the upcoming adoption of delegated and implementing acts.

Bird & Bird

Bird & Bird offers comprehensive support related to the new obligations under the CBAM. Our team has already supported clients assess the impact of the CBAM while the legislative process was still ongoing. We also have broad experience in related fields – EU ETS compliance, and advice on cost optimization and indirect cost compensation.

For further details or should you have any questions, please contact Grzegorz Pizoń and Tomasz Chabrzyk.

{kind=link}